文章

Offshore Fund Exemption Regime for Hong Kong-domiciled Funds (英文版本)

暂时只提供英文版本

Practice Note (DIPN) 61 to provide clarification on its view on offshore fund exemptions for Hong Kong–domiciled funds. While the offshore fund exemptions initially only applied to non-resident funds, effective from 1 April 2019 these profits tax exemptions also became applicable to Hong Kong–domiciled funds.

Four main areas of exemption are covered in DIPN 61, as listed below:

Definition of fund: a person has to be qualified as a ‘fund’ in order to enjoy the offshore fund exemption

Exemption provisions: fund, special purpose entities and private companies

Anti-round tripping provisions: deeming provisions

Incidental transactions

In this article we will mainly focus on the first two areas, since radical changes have been implemented in comparison with the previous provisions, while only limited changes have been made to the latter two areas.

Definition of fund

The definition of ‘fund’ is similar to that of ‘collective investment scheme’ under the Securities and Futures Ordinance (SFO). The fundamental principle behind the definition is to prevent the abuse of offshore fund exemptions when investors are making the investment on their own, rather than relying on asset management services from external service providers, as the exemptions are intended to promote the development of the asset management industry in Hong Kong.

The IRD will look at all relevant decisions in judging whether a person is a fund or not (a detailed definition of ‘fund’ is given in Section 20AM of the Inland Revenue Ordinance (IRO)). Before providing some insights, we must stress that a person has to fulfil the definition of fund at all times during the year of assessment in order to qualify for any profits tax exemption.

The central tenet is that the investors (that is, participating persons) do not have day-to-day control over the management of the fund, as a fund should be managed as a whole by a fund operator (for example, a corporation licensed by the Securities and Futures Commission) that has overall responsibility for the management of the fund, including investment advice and operational services. A securities broker, for instance, is unlikely to be considered a fund operator as it merely carries out the investment decisions of its clients, instead of providing investment advice.

On the other hand, an arrangement intended to have only one investor would not normally be considered a fund as it is unlikely to fulfil the ‘pooling’ requirement. For some complex structures, such as parallel funds or a master-feeder structure, it is important to look at all the relevant facts – including whether such funds constitute separate funds or not – before determining if the structure falls under the definition of fund as set out in Section 20AM of the IRO.

Lastly, the IRD has also highlighted that group schemes or employee share schemes, in which the operations are in the same group of companies, would not generally fall under the definition of fund, as the taxability of employee remuneration in Hong Kong cannot be exempted under a fund structure.

Exemption provisions

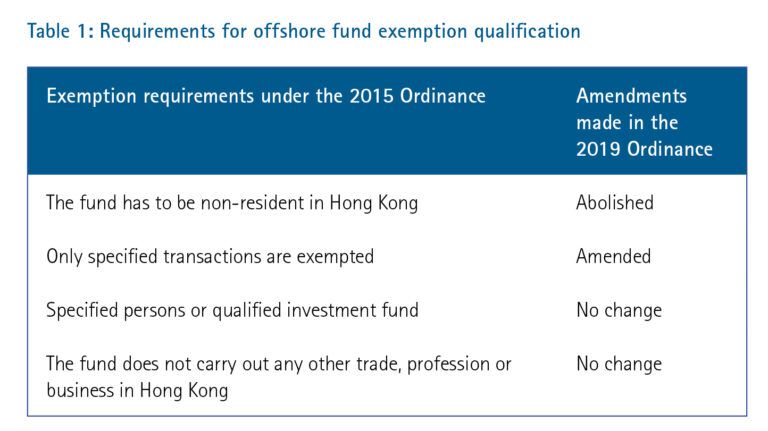

To begin with, Table 1 highlights the four main requirements for a fund to be qualified for an offshore fund exemption under the Inland Revenue (Amendment) (No 2) Ordinance 2015 (2015 Ordinance) and what amendments, if any, were made to those requirements in the Inland Revenue (Profits Tax Exemption for Funds) (Amendment) Ordinance 2019 (2019 Ordinance).

We will now go through each requirement in turn.

Non-resident in Hong Kong

Under the 2015 Ordinance, a fund had to be a non–Hong Kong resident in order to qualify for an offshore fund exemption. Under the 2019 Ordinance, Hong Kong–domiciled funds are now also eligible for offshore fund exemptions but are subject to additional requirements, which will be further discussed below in the section on specified transactions.

The tax residency of a fund generally refers to the location in which the central management and control of the fund is exercised – the place of incorporation is not the deciding factor when determining tax residency. Rather, when examining the location of management and control, the IRD will look at a number of other factors, including the location of directors and where the board of directors’ meetings take place. Obtaining a Certificate of Resident Status in Hong Kong demonstrates that the IRD confirms an entity is a Hong Kong tax resident. For further details about Hong Kong tax residency, please refer to our article in the December 2019 edition of CSj.

Specified transactions

Specified transactions include, amongst others, transactions in public securities, private company shares, futures contracts and foreign currencies. Of these, transactions in private company shares are attracting the most attention in the market, particularly those relating to the private equity industry.

For transactions in private companies, it is common practice for a fund to set up one or more special purpose entities (SPEs) to hold the investments in the investee private company (PE). In the following section, we will discuss the exemption requirements for SPEs and PEs.

Special purpose entities. The requirements for SPEs remain substantially the same as those in the 2015 Ordinance. An SPE must be established for the sole purpose of holding and administering a private company and is not allowed to carry out any other trade or activity after incorporation. In particular, an SPE is only permitted to conduct the following business activities:

• reviewing the financial statements of portfolio investment companies

• attending shareholder meetings of the portfolio investment companies

• opening bank accounts to enable the receipt of dividends and investment disposal proceeds, and

• appointing a company secretary and auditor.

Private companies. Under the 2015 Ordinance, offshore fund exemptions were not granted to funds investing in a private company incorporated in Hong Kong. These exemptions were extended

in the 2019 Ordinance to include investment in Hong Kong private companies, but such investments are subject to additional requirements.

In contrast, the limitation on investment in Hong Kong immovable property still applies. In particular, whether considering the private company itself or the companies in which the private company has invested, the aggregate market value of the holding of immovable properties in Hong Kong cannot account for more than 10% of the total asset value of the respective company.

Despite the fact that market value will be applied in the 10% threshold, the IRD will first make reference to the book value in the audited financial statements of the private company. As such, it is recommended to limit both the book value and the market value of any Hong Kong immovable properties to the 10% threshold.

As mentioned above, offshore fund exemption has been extended to Hong Kong private companies. However, as the intention is to encourage the fund to hold private companies for long-term investment purposes, Hong Kong private companies are subject to one of the following additional requirements:

• the fund has to hold the private company for at least two years

• the fund does not have a controlling shareholding of the private company, and

• no more than 50% of the market value of the assets of the private companies are short-term assets (that is, the holding period of

the relevant assets is less than three years).

• As long as one of the above three conditions is satisfied, the exemption will apply to private companies in Hong Kong.

Specified persons or qualified investment fund

Exemptions are made available to a fund if that fund is carried out or arranged by a specified person in Hong Kong, or if the fund qualifies under the definition of a qualified investment fund. The term ‘specified person’ generally refers to a licensed corporation under the SFO, while to be classified as a ‘qualified investment fund’, the following conditions must be met.

• the number of investors (excluding the originator and the originator’s associates) exceeds four at all times after the final closing

of sale of interests

• over 90% of the aggregate capital commitment is made by investors (excluding the originator and the originator’s associates) at

all times after the final closing of sale of interests, and

• net proceeds to be received by the originator and the originator’s associates cannot exceed 30% (after deducting the portion that

is attributable to them based on their capital contribution).

Paragraphs 82 to 94 of DIPN 61 provide more detailed definitions of some of the specific terms mentioned above.

Anti-round tripping provisions

Anti-round tripping provisions are substantially the same as the deeming provisions defined in the 2015 Ordinance. Even when a fund meets all the above exemption requirements, a deemed taxable income will be imposed on Hong Kong investors of the fund in the following situations:

• if the Hong Kong investors jointly hold 30% or more of the beneficial interest in the fund, or

• if Hong Kong investors who are associated with the fund hold any beneficial interest in the fund.

Having said the above, anti-round tripping provisions do not apply under the following situations:

• when, at all times during the year, 50 or more persons hold all the units of the fund

• when, at all times during the year, 21 or more persons are entitled to 75% or more of the income or property of the fund, or

• by special concession by the IRD’s assessor.

Incidental transactions

Incidental transactions represent transactions incidental to the carrying out of specified transactions. Typical examples of incidental transactions are interest or dividend income on securities and custody of securities.

If the trading receipts from incidental transactions do not exceed 5% of the total trading receipts (both specified transactions and incidental transactions), the incidental transactions could still be exempted. On the contrary, if the trading receipts from incidental transactions are over the 5% threshold, the total amount of the trading receipts from incidental transactions is subject to Hong Kong profits tax.

Having said the above, it is worth noting that some of the trading receipts from incidental transactions (for example, dividend income or offshore interest income) are non-taxable in Hong Kong even without the exemption.

Last piece of advice

While the HKSAR Government is dedicated to promoting both the asset management industry in Hong Kong and Hong Kong–domiciled funds, the IRD has expressed concern about the potential abuse of offshore fund exemptions, especially on short-term trading of Hong Kong securities, as capital gains from long-term investments – as well as income from overseas securities – are likely to be non-taxable in Hong Kong.

It is therefore important for the fund administrator to pay close attention to all the above requirements, as failure to comply with any one of the requirements, even for a short period of time during the year, may render the fund ineligible to enjoy the exemption benefits